- home

- News

Latest News

May 7, 2026

Paytm turned in yet another profitable quarter in Q4. Buoyed by growing revenues, expenses under control and core payments vertical doing most of the heavy lifting, the fintech major posted its first full fiscal FY26 in the black.

turned in yet another profitable quarter in Q4. Buoyed by growing revenues, expenses under control and core payments vertical doing most of the heavy lifting, the fintech major posted its first full fiscal FY26 in the black.

Here is a quick snapshot of Paytm’s Q4 FY26 numbers:

Profit With Discipline: The headline numbers vindicate Paytm’s thesis. The full-year profitability and positive EBITDA swing imply steadier operating leverage and tighter cost control. The lean structure was also a direct result of AI-led automation, which helped the company trim indirect expenses and increase efficiency.

Payments In Driver’s Seat: The core payments vertical continued to anchor the story. Merchant GMV rose sharply, monthly transacting users remained high, and transaction volumes continued to expand, showing that Paytm still has scale on its side. The expansion of merchant subscriptions and device-led distribution also gave the company more monetisable touchpoints.

The Wealth Tech Engine: The financial services arm continued to be the fintech’s growth engine. It continued to leverage its base of 7.7 Cr monthly transacting users to cross-sell high-yield credit and EMI products. This was reflected in the payment processing margins, which jumped to over 4 bps in Q4 as higher-margin instruments such as credit cards and EMI products gained market share.

FY27 Roadmap: Going forward, Paytm expects revenue growth to accelerate further in the ongoing fiscal, alongside continued expansion in EBITDA margins, driven by operating leverage and growth across its verticals. While it would be interesting to see if the momentum continues going forward, for now, here is how Paytm fared on the financial front in Q4…

India’s blue-collar economy depends on migrants who move cities for better pay, but many cannot stay because urban living is too expensive and too uncertain. Nia.one is trying to fix this gap by bundling housing, meals, jobs and support into a one worker-first platform.

The Niadel Model: Founded in 2024, Nia.one operates at the intersection of livelihoods and urban infrastructure. The startup’s physical hubs, called Niadels, are set up near industrial clusters in metros. Each site offers no-deposit accommodation, meals, groceries, laundry and optional upskilling, while also helping workers move between jobs without losing income.

A typical worker earning around ₹15,000 a month can keep enough after rent, food and essentials to send about ₹8,000 home, which is the core promise behind the model.

A Layered Business: Nia monetises both workers and enterprises. While it earns on rent, food and grocery margins, the startup also charges staffing commissions from employers. The company is also building financial services and an AI assistant called Rafiki to improve job matching and spending decisions.

Scaling The Ecosystem: Backed by Elevar Equity, the startup closed FY26 with an ARR of ₹30 Cr. Going forward, Nia.one plans to add 5 Lakh members across its nearly 3,000 centres, up 50X from 10,000 currently. With a Series A fundraise on the cards, can Nia.one disrupt India’s gig economics?

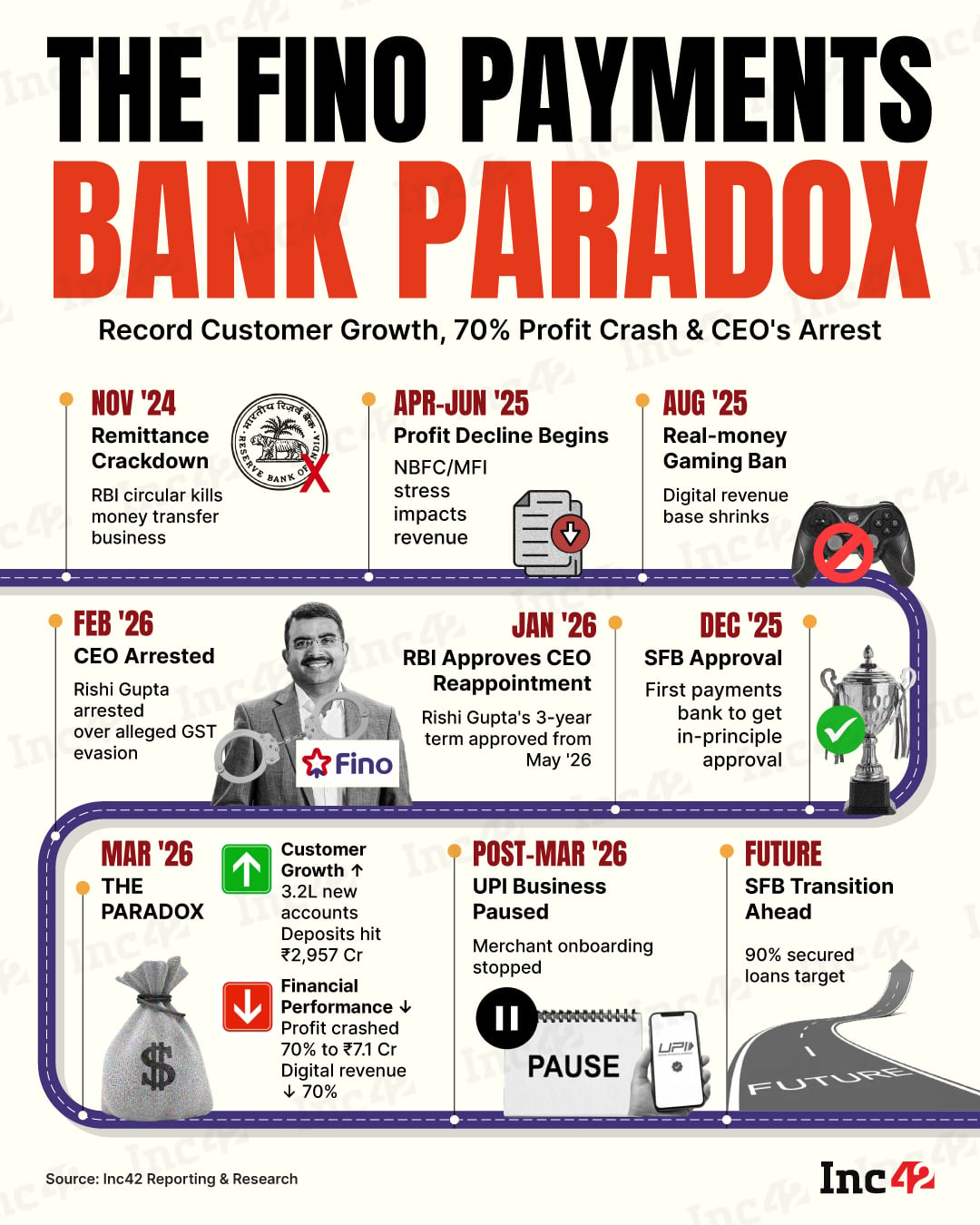

Fino Payments Bank added 3.2 Lakh new accounts in March 2026, its highest monthly growth in three years. So, how does the payments bank face a CEO arrest, regulatory crackdowns and business shutdowns, yet see record customer acquisition?