- home

- News

Latest News

February 8, 2026

India’s consumer services giants are enduring a winter of discontent. From ride-hailing drivers to quick commerce riders, gig workers are protesting over shrinking payouts and gruelling schedules.

The latest one came over the weekend, as drivers associated with Uber, Rapido, Ola, and Porter staged a nationwide protest over minimum fares and restrictions on the use of private vehicles for commercial rides.

In the same week, gig workers associated with Urban Company, Zomato, Zepto, Swiggy Instamart also raised similar concerns through collective strikes in Delhi NCR, and other cities.

Instamart also raised similar concerns through collective strikes in Delhi NCR, and other cities.

These are not isolated episodes. Such has been the clamour and the intensity of these back-to-back strikes that the issues related to gig workers have echoed in the Parliament, too. The aftermath has been swift, as many platforms are now forced to withdraw their 10-minute delivery claims.

Yet, despite the rising regulatory attention and the formal recognition of gig work, dissatisfaction keeps resurfacing. On the surface of it, the answer to the problems facing gig workers seems simple – increase payouts, extend timelines and extend more social welfare incentives.

But the reality is not so black and white and reveals a complicated aggregator-side tale — a perspective which inspired today’s edition of The Outline.

To be true, online aggregators operate in a survival mode: thin margins, relentless competition, and a constant push to keep expanding. Under these conditions, coughing up more can become a compounding cost at scale.

In a week headlined by a gig workers’ strike, the real story sits beneath the headlines. To understand why these protests keep returning and why aggregators struggle to respond, it is necessary to examine the structural role of the gig economy in India and the financial realities that underpin it.

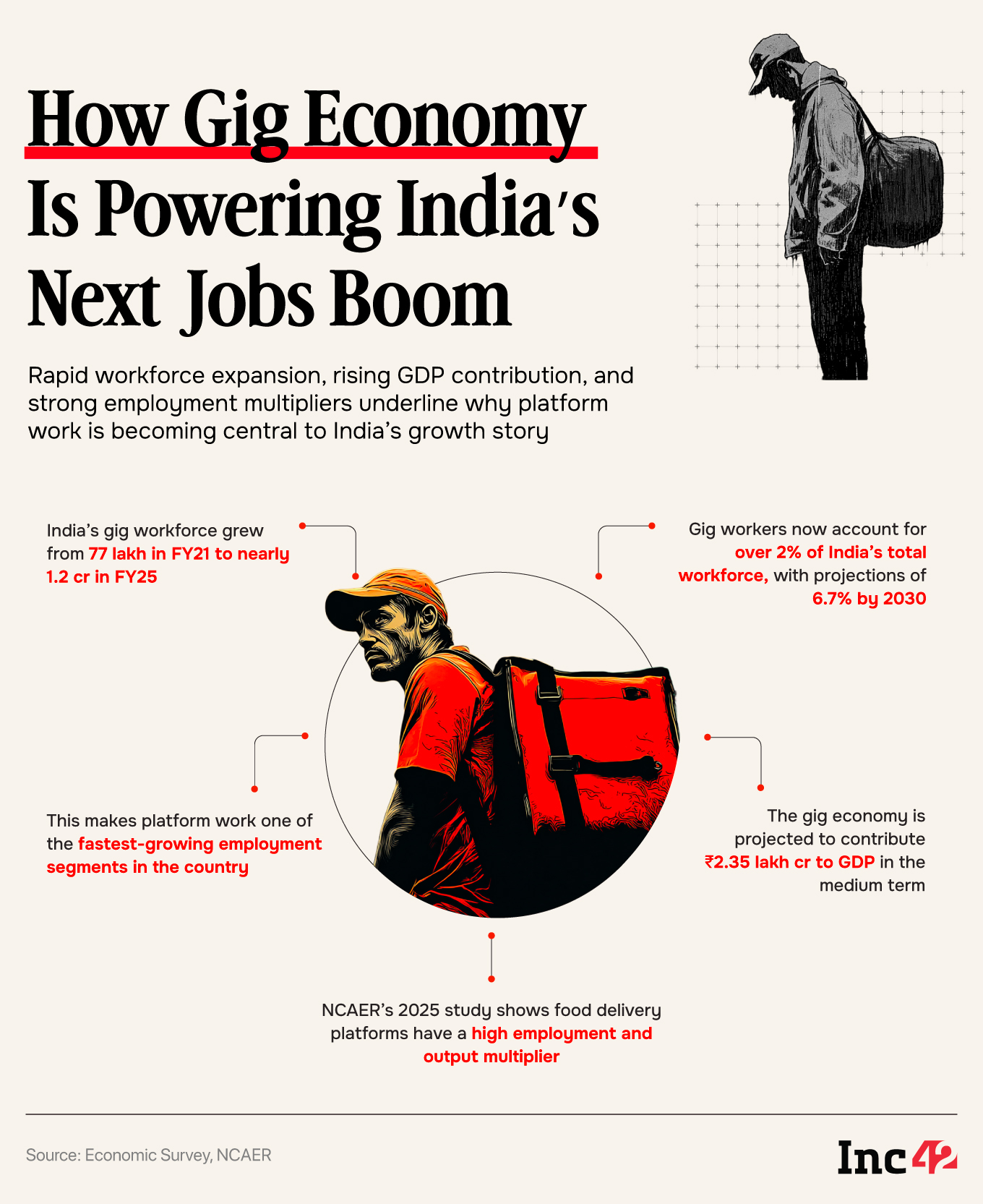

India’s gig workforce has expanded rapidly over the past few years. According to the Economic Survey 2025-26, the number of platform workers increased from 77 Lakh in FY21 to nearly 1.2 Cr in FY25, accounting for over 2% of the country’s total workforce now. The sector is projected to contribute around INR 2.35 Lakh Cr to GDP by the end of the decade.

This growth has been driven by rising smartphone penetration, UPI adoption, and the proliferation of hyperlocal delivery and mobility platforms. But beyond headline numbers, platform work has played a deeper structural role in India’s labour market.

Multiple studies, including the National Council of Applied Economic Research’s (NCAER) assessment of food delivery workers and recent NBER research, show that for most participants, gig work functions as a transitional job rather than a long-term career.

Workers enter platforms after job losses, during economic slowdowns, or while pursuing education. Many eventually exit for better-paying formal roles. In this context, the gig work operates as a shock absorber, providing temporary income stability in a volatile labour market.

And because gig work is largely temporary, worker dissatisfaction is built into the system. Further, as living costs rise and incentives fluctuate, income becomes a recurring trigger for unrest.

On the surface, these platforms appear well-funded, heavily advertised, and deeply embedded in urban life. But financially, most operate under fragile unit economics. Despite years of funding and scale, many delivery and quick commerce firms remain loss-making or marginally profitable.

Their financials and investor disclosures consistently show high spending on logistics, discounts, and customer acquisition. Even small changes in per-order payouts could have a disproportionate impact at scale.

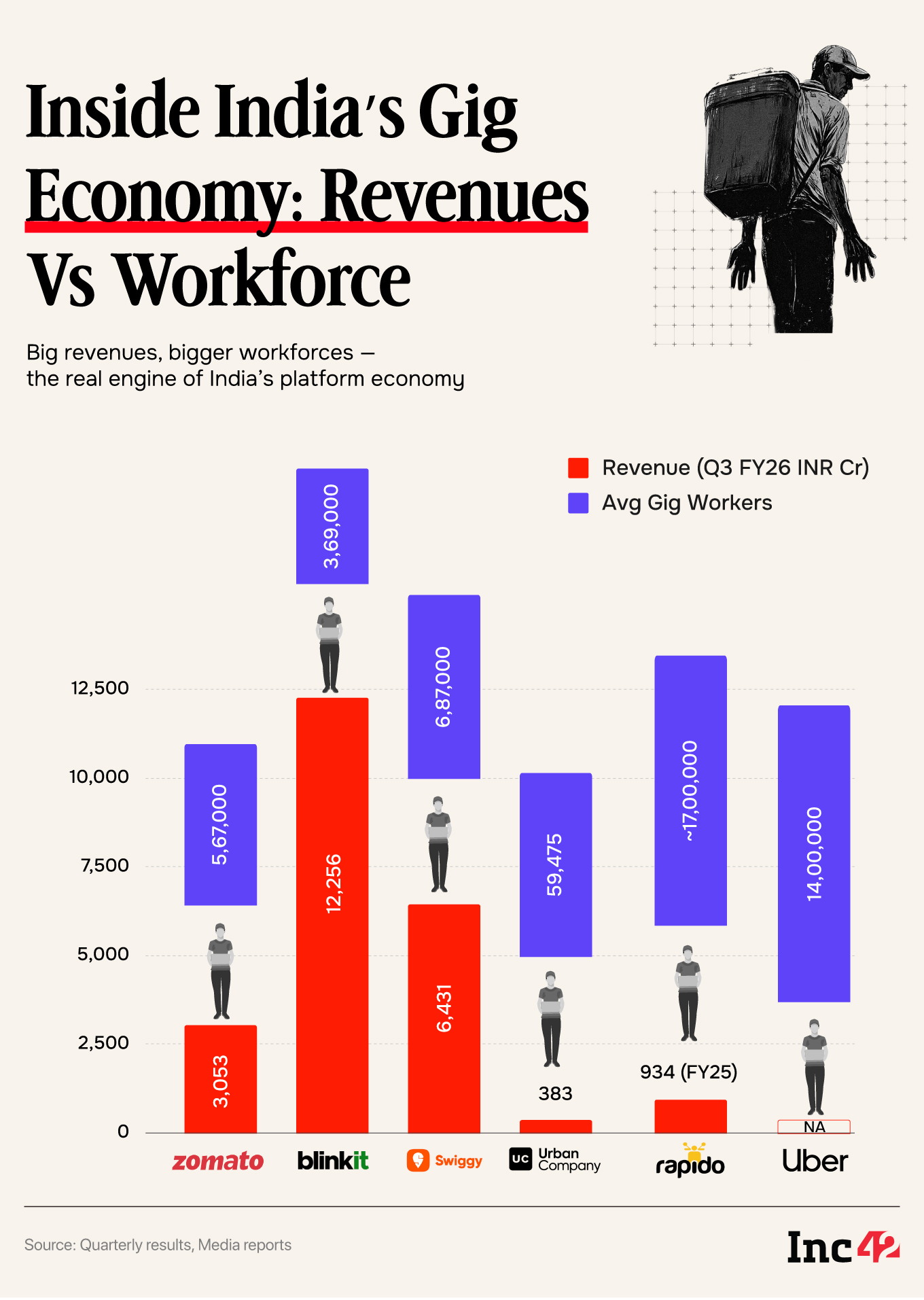

For instance, a ₹5 increase in per-order rider incentives, multiplied across millions of monthly orders, can translate into hundreds of crores in additional cost annually. For context, in Q3 FY26, Blinkit clocked 24.3 Cr orders while Swiggy delivered 29.4 Cr orders.

In aggregator businesses where contribution margins often range in low single digits, this is not a trivial adjustment.

Therefore, it goes without saying that a strike is the last thing these platforms want to afford, as strikes, irrespective of their size, create an operational hurdle for companies, impacting their revenues. Protests also leave a poor user experience and result in the platform losing customers.

Then, most platforms are still in expansion mode. While metro markets like Delhi, Mumbai, and Bengaluru generate relatively stable volumes, companies are aggressively expanding into tier II and tier III cities. These markets typically have:

As a result, operations in smaller cities are often loss-making in early years. To fund this expansion, platforms rely heavily on surplus generated in metro markets. This cross-subsidisation model leaves limited room for pay hikes across the board.

This financial strain is also visible in a slew of new charges. Over the past two years, most aggregators have either rolled out or increased platform fees, rain surcharges, late-night fees, and distance-based pricing – all aimed at improving unit economics.

Besides placating investors, these revenue streams are also utilised to offer shelter or resting areas and other facilities to delivery executives. Recently, Albinder Dhindsa, Group CEO of Eternal, said that Blinkit was offering free medical checkups for its delivery executives.

Aggregators have also been using these additional costs billed to customers to offer some form of insurance to gig workers for years now. However, gig workers still seem to be up in arms and seek better insurance options.

“The nature of the work is such that a platform is not accountable to provide them with accident cover or health cover or any of that. Instead, such protections are meant to be delivered through a central government social security scheme. While the relevant Social Security Code was legislated in 2020, it was only notified in November 2025. The detailed rules were released on December 30, 2025, and have been placed in the public domain for a 45-day consultation period,” said Rishi Agarwal, the cofounder and CEO of Teamlease Regtech.

Another major constraint for aggregator profitability is India’s discount-reliant consumer base. Delivery and quick commerce platforms rely heavily on discounts and promotions to drive adoption. Cashbacks, free deliveries, and deep price cuts have become the primary tools for customer acquisition.

While this strategy has helped platforms scale quickly, it has also created long-term structural problems. By consistently offering subsidised prices, aggregators have trained users to expect convenience at artificially low costs.

Over time, this has weakened the ability of the entire ecosystem, from ride-hailing apps to quick commerce giants, to sustain aggressive discounting. Economists refer to this as weak pricing power, which is the inability to raise prices without losing customers.

In practical terms, this means:

As a result, even when platforms want to increase worker payouts, they lack the pricing flexibility to fund it.

An often overlooked factor in the debate around gig workers’ income is consumer behaviour. In many developed markets, tipping forms a meaningful portion of delivery workers’ earnings. In India, however, this behaviour is rare.

Industry surveys suggest that only 3-5% of users regularly add tips, and even then, the amounts are usually nominal. For most workers, tips contribute little to the overall income.

This lack of tipping creates a vicious loop, which places the entire burden of compensation on platform payouts even as consumers consistently prioritise low prices over service sustainability.

With customers unwilling to pay slightly higher prices for fair labour costs, platforms have limited room to restructure payouts. This results in worker incomes being shaped not only by company policies but also by consumer expectations.

Taken together, these structural factors explain why worker protests remain cyclical. Most research converges on one conclusion – long-term stability in the gig economy depends less on short-term pay hikes and more on structural reforms, which include:

As NCAER and NBER studies show, many workers who exit platforms successfully transition into better-paying roles when supported by skills and experience. In that sense, the gig economy works best as a stepping stone, not a permanent solution.

All said and done, until platforms achieve sustainable profitability and consumers accept the convenience has a price attached, tensions between delivery and gig workers and platforms will likely endure.

Edited By Shishir Parasher

Creatives By Abhyam Ghusai